One Billion and Rising, but Not Evenly: How Africa’s Startup Scene Grew Up in 2025

A Symbolic Milestone with Uneven Distribution

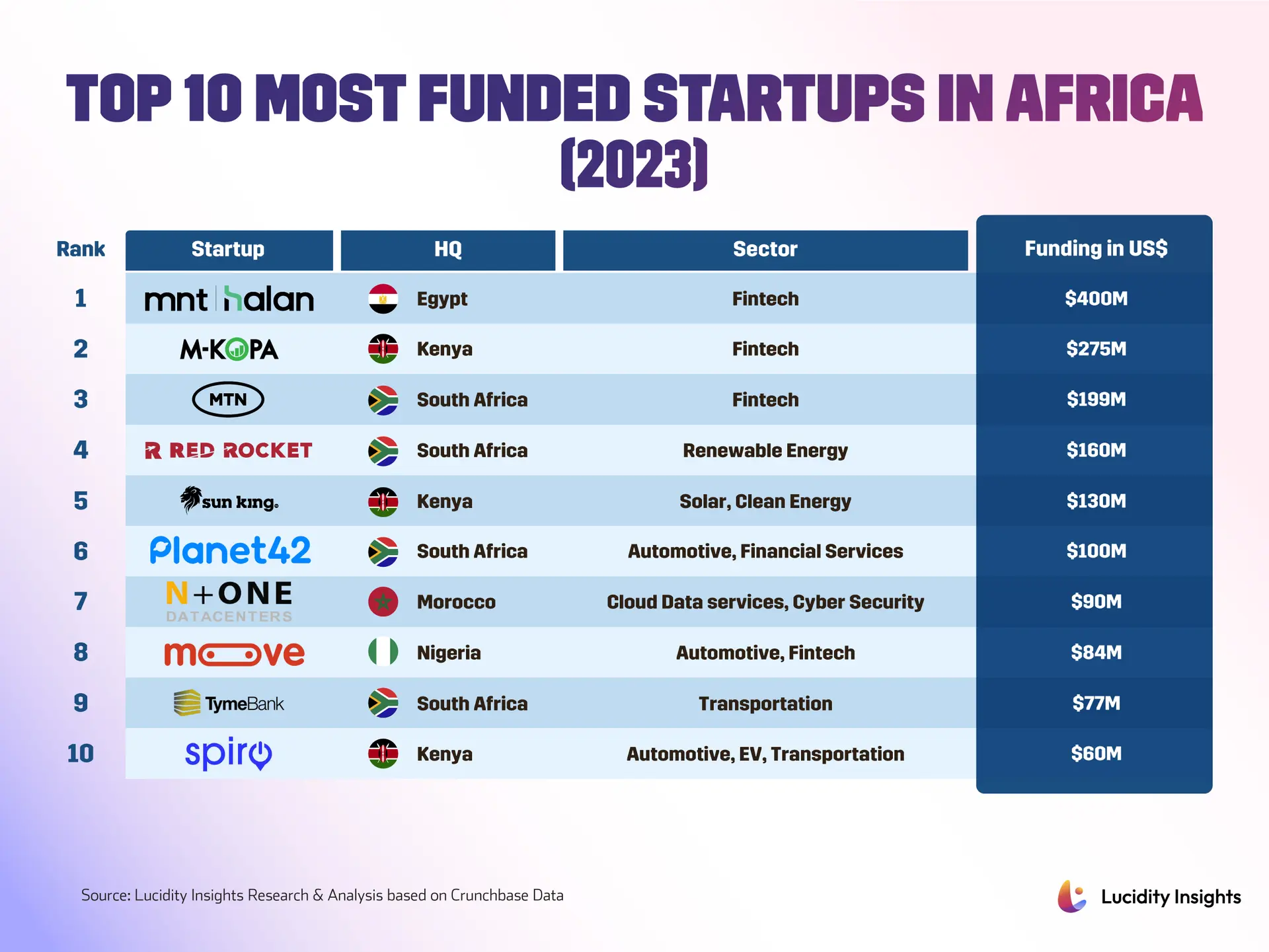

Africa’s startup ecosystem hit a symbolic milestone in 2025, with companies across the continent raising more than one billion dollars between January and May alone. That’s a jump of about 40 percent from the same period in 2024, according to recent funding reports. The surge captures a trend that began back in 2019, when investors started reassessing long held assumptions about African markets. But here’s the thing, the headline numbers tell one story while the distribution beneath them tells another. Most capital continues flowing into the so called Big Four, Nigeria, Kenya, South Africa, and Egypt. Yet 2025 really underlined Egypt’s breakout moment. Reported funding into Egyptian startups more than doubled year on year, with roughly $330 million raised in the period and a cluster of large deals. Proptech firm Nawy led the pack with a headline grabbing raise, while fintech names like Valu, Thndr, and Money Fellows also captured sizeable rounds. Those deals signal investors’ appetite for consumer financial services and property technology that can scale quickly across dense urban markets. Beyond the capitals, quieter shifts are underway too. Emerging markets like Ghana, Tanzania, Senegal, Ivory Coast, and Tunisia are attracting attention, even if total dollar volumes remain modest by comparison. Local founders, regional funds, and development finance are beginning to stitch together an ecosystem that can support more than the usual handful of high profile winners, as highlighted in our coverage of Africa’s startup boom.

Growing Pains and Investor Scrutiny

But let’s be real, the bounce in funding hasn’t erased the strain. 2025 was a year of sobering exits and restructurings as well as fresh money. In East Africa, the consumer credit and buy now pay later sector hit turbulence when Lipa Later, a Kenyan BNPL startup, entered administration in March after struggling to raise follow on capital and to manage debt and payroll obligations. Buy now pay later, a short term credit model that splits purchases into installments, can fuel rapid adoption but also leaves lenders exposed if repayment weakens, especially as market corrections and higher funding costs tighten the environment. That caution is visible across sectors. Several startups have cut staff or pivoted under investor pressure, and investors are demanding clearer paths to profitability rather than growth alone. Headlines about layoffs and tightened due diligence have become part of the narrative, signaling that capital is still available, but at a higher bar. For founders this means stronger unit economics, diversified revenue streams, and robust risk management aren’t optional anymore. The mix of headline deals and hard lessons is reshaping how capital flows. Institutional players and international development banks are still active, and deals like large bond issuances and regional financing packages show appetite for backing infrastructure and cross border scaling. Meanwhile, private venture rounds continue landing in fintech, logistics, and e mobility, the latter attracting record investments in 2025 as investors bet on solutions for transport, trade, and last mile delivery. This evolving landscape reflects what industry analysts have been tracking closely.

Diversity, Constraints, and What Comes Next

Sector diversity matters because it spreads systemic risk. When funding concentrates in consumer credit, a shock to incomes or to underwriting models can ripple quickly. Conversely, growth in proptech, agritech, and B2B software points to opportunities tied to real assets and trade flows, which can be more resilient through cycles. Policy and infrastructure remain recurring constraints though. Electricity, digital payments rails, and harmonized regulation across African markets affect how quickly startups can scale. At the same time, regulators are tightening scrutiny where consumer protection or systemic risks appear, and investors are noticing. The outcome will likely be a period of consolidation, where stronger teams, clearer unit economics, and compliant operations win larger, more sustainable rounds. For investors the calculus is shifting from pure market potential to execution and governance. Some backers are leaning into longer term, programmatic support that includes governance help and operational lifts. Others are rebalancing by geography, exploring underfunded markets where valuations are lower and local networks can create privileged access to deal flow. What comes next is a test of maturation. The industry needs more exits that reward early stage backers, and that will require IPOs, cross border acquisitions, or deeper secondary markets. It also needs a stronger local investor base to reduce dependence on international capital cycles. If 2025 showed the upside of renewed interest, it also made clear that the future will favor startups that are disciplined on growth, creative on business models, and rigorous on risk. Looking ahead, there’s reason for cautious optimism. The money flowing into Africa is larger and more varied than in past cycles, and innovation is spreading beyond capital cities, as seen in the broader tech renaissance across the continent. But the next phase will be defined by whether startups can translate scale into sustainable profitability, and whether policy makers, development banks, and private investors align to build the infrastructure and regulatory certainty that scaling businesses require. Expect the pace of deals to remain brisk, yet more selective, with 2026 likely to be a year of strategic consolidation, smarter capital deployment, and, potentially, a new generation of African companies ready for global markets. For ongoing coverage of these developments, TechCrunch’s Africa section provides regular updates, while our own analysis of Africa’s digital transformation offers deeper insights into the continent’s evolving tech landscape.