Africa’s Tech Reset: 18 Startups Poised to Revive Funding and Hunt for 2026 Unicorns

After a bruising 2025 that produced no new tech unicorns and saw startup shutdowns jump by half, Africa’s technology scene is quietly regrouping. Investors pulled back, equity deals cooled, and roughly $52 million in investor capital evaporated as weaker companies closed their doors. Yet beneath that headline turbulence, new financing patterns, maturing sectors, and a concentrated list of scale-ready firms are creating a clearer runway for growth in 2026. Analysts and investors are now watching about 18 companies across fintech, energy, mobility, healthtech and property, businesses that may either reach billion dollar valuations or pursue public listings next year. The pause in mega-rounds has driven a shift in behavior. Venture capital remains important, but structured credit and securitized instruments are filling gaps. Securitized financing means a company bundles expected future revenues or assets and sells them to investors, converting long-term cash flows into up-front capital. For capital-heavy energy players that model fits better than chasing headline-grabbing private valuations. This shift reflects a broader maturation of Africa’s startup ecosystem that we’ve been tracking closely.

Where the Action Is Heating Up

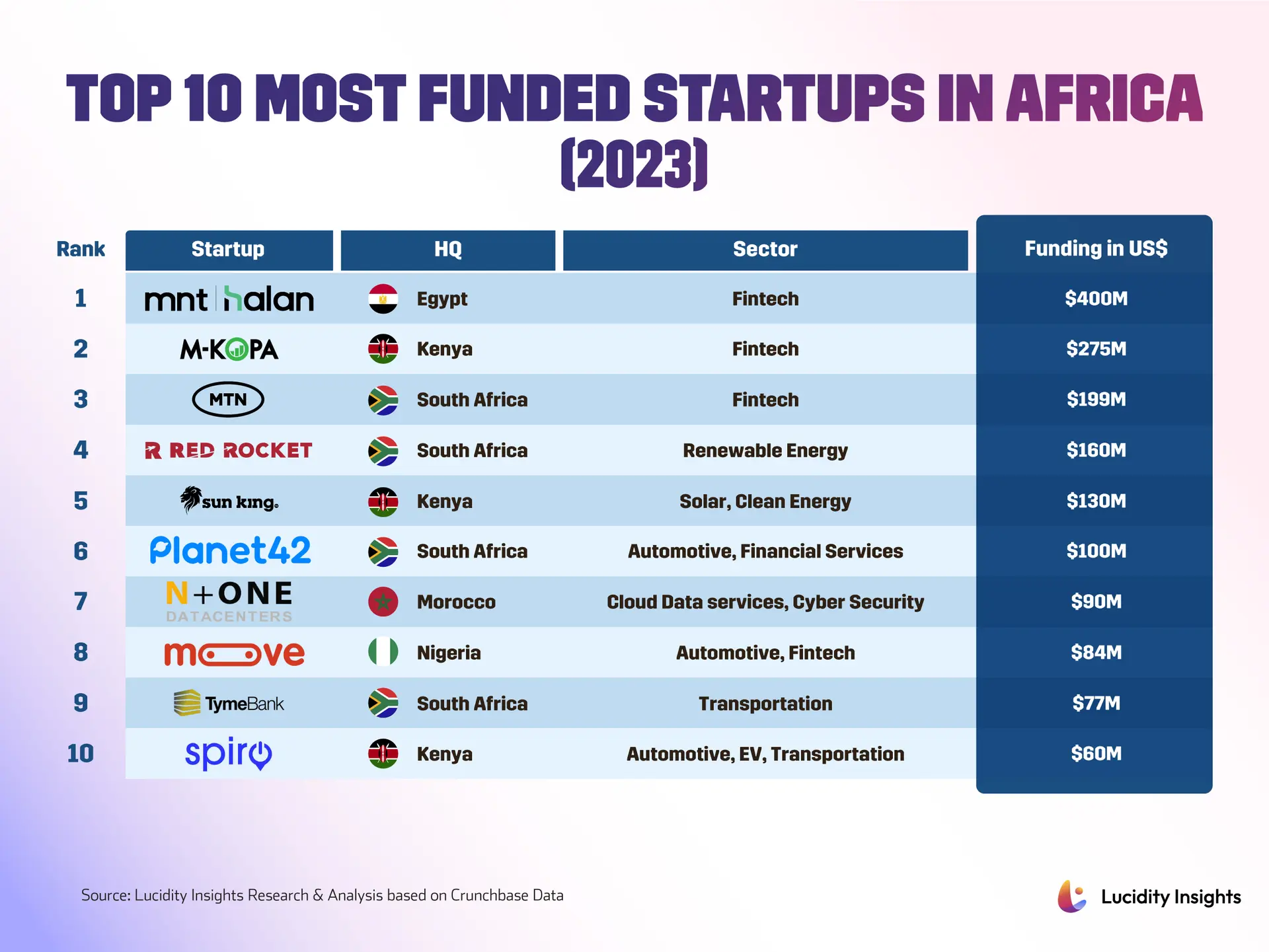

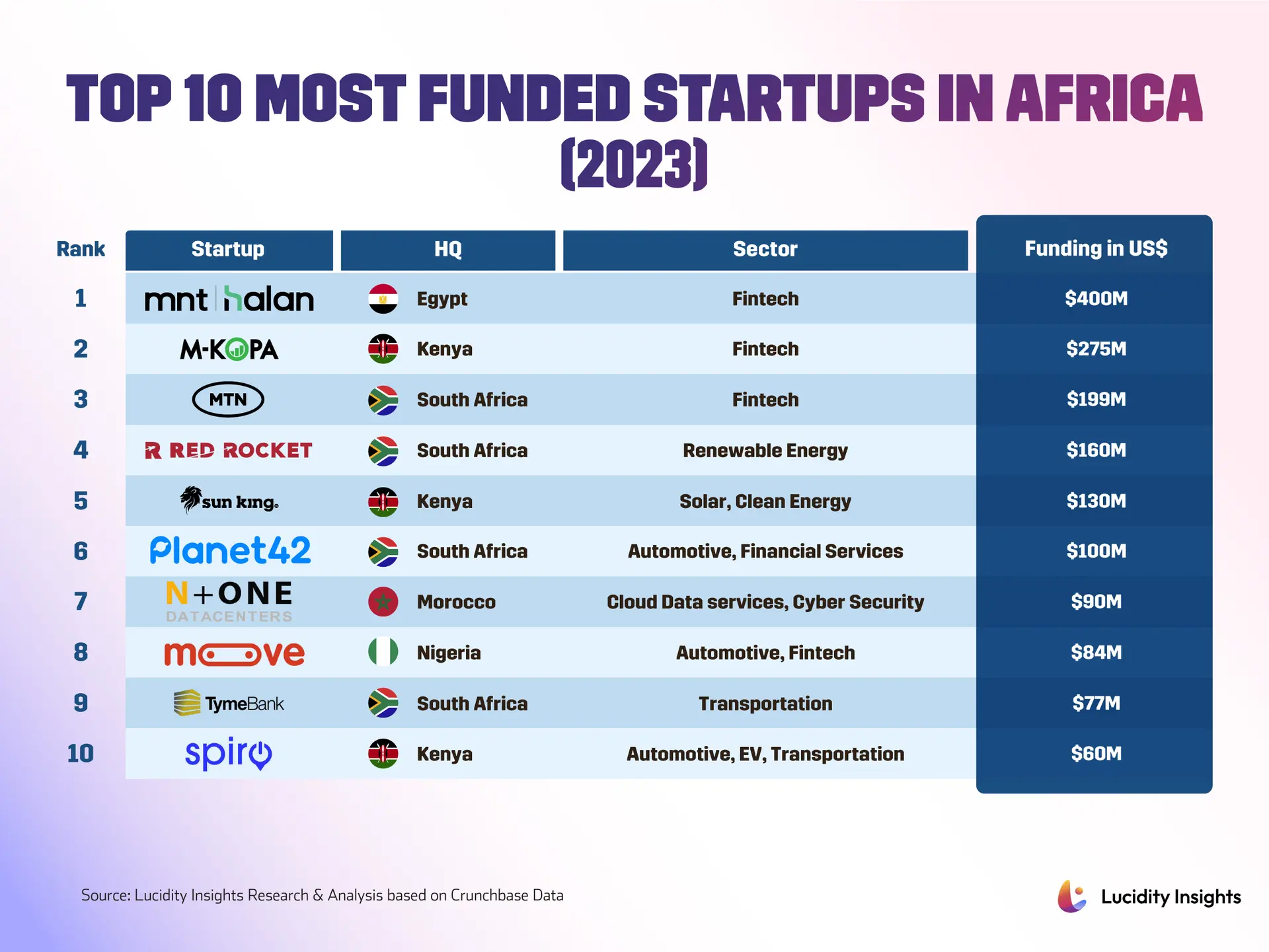

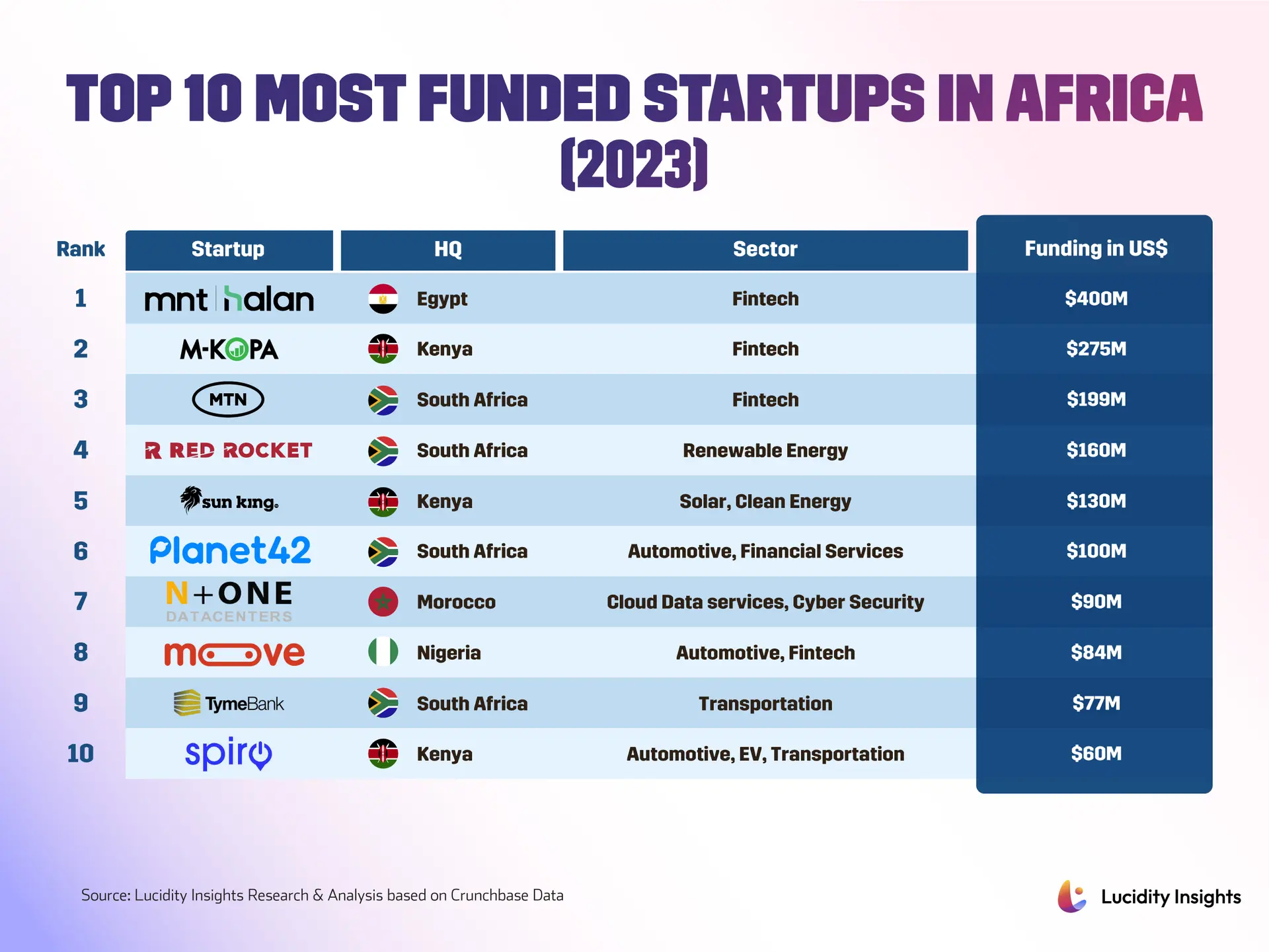

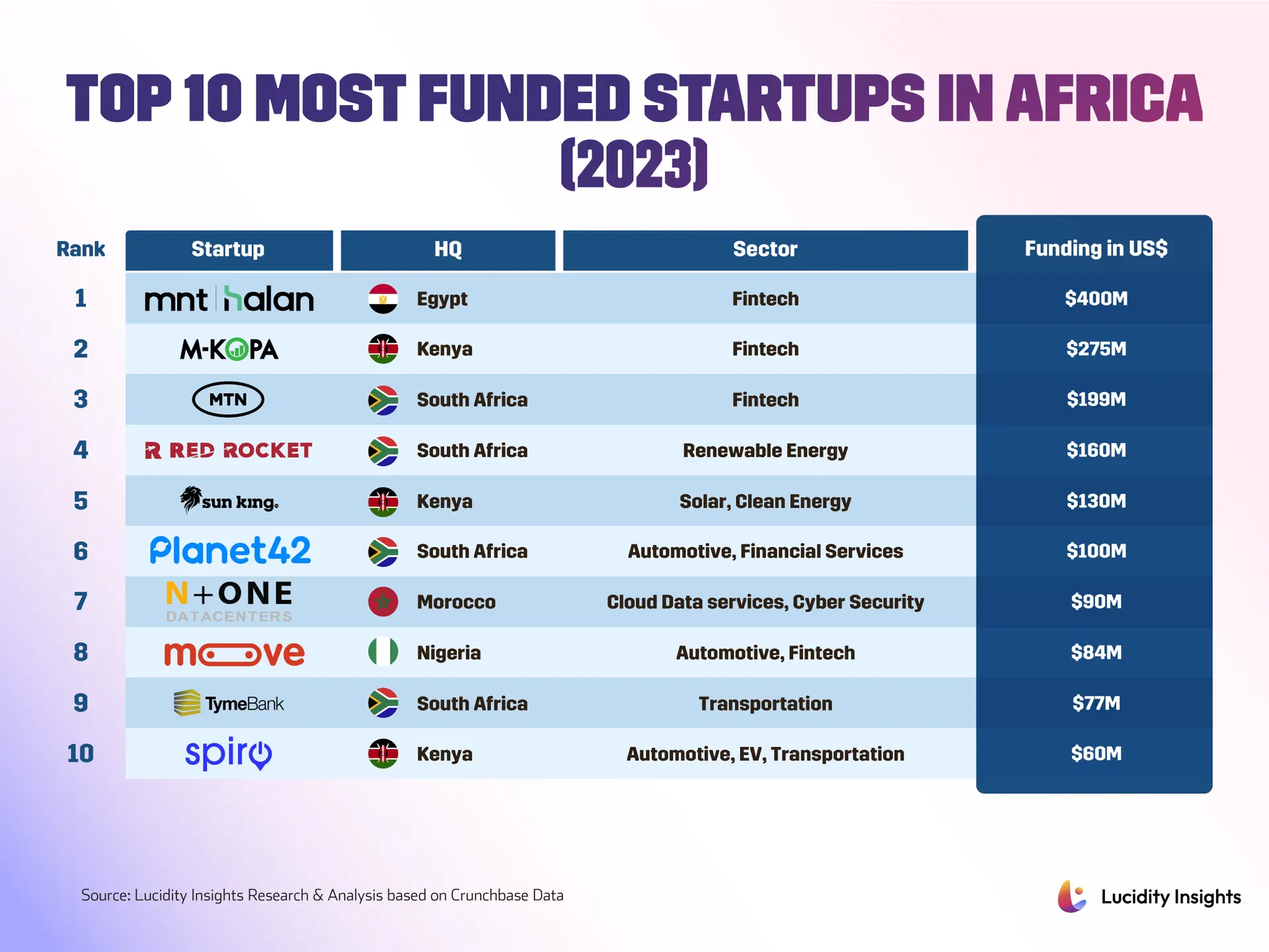

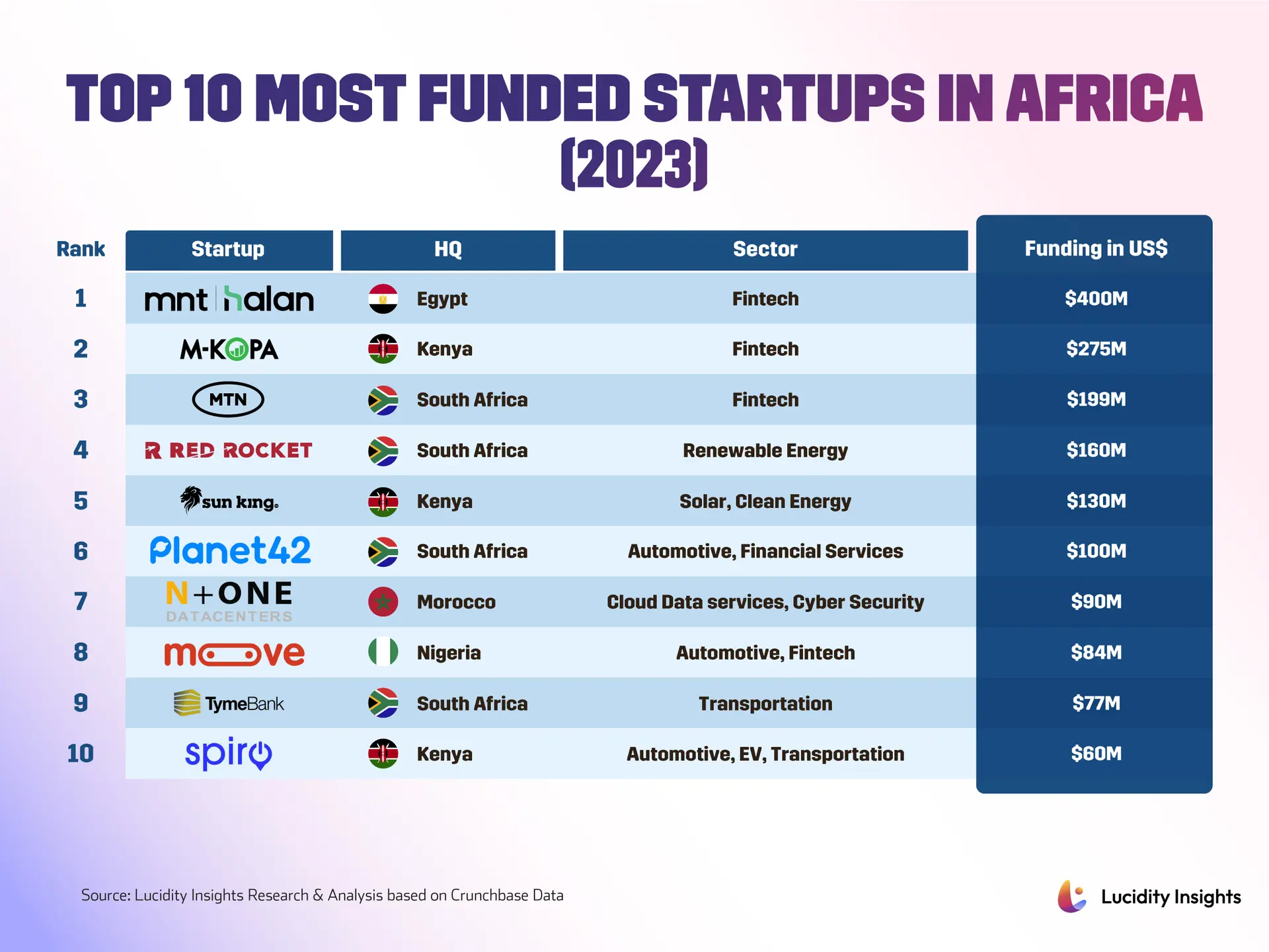

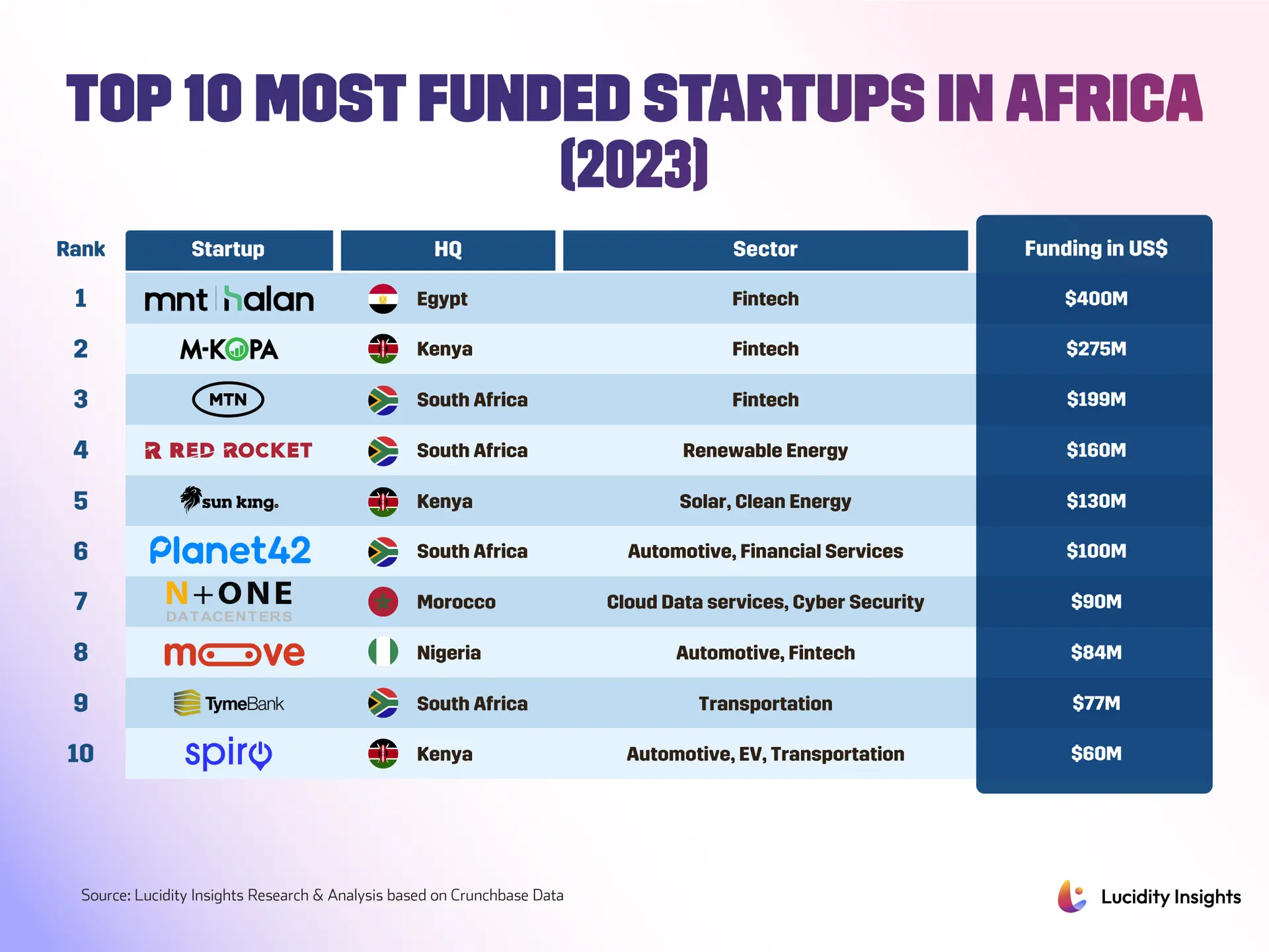

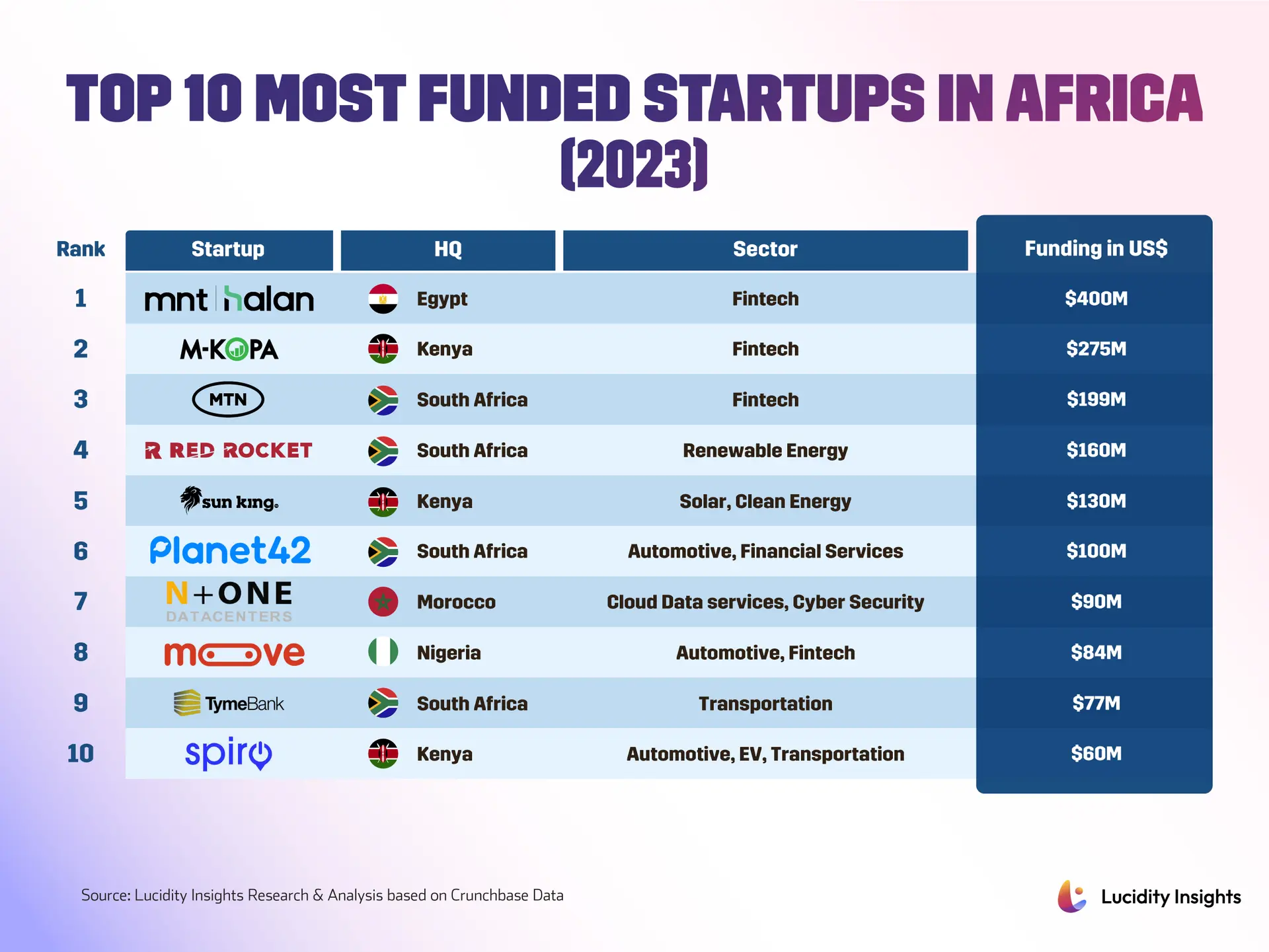

Energy firms are leading this maturity wave. Companies such as Sun King and d.light leveraged that shift, tapping structured and securitized markets while Sun King also closed a $40 million equity round late in 2025. SolarSaver and PowerGen, which raised more than $50 million during the year, are among others now viewed as potential scale leaders. These firms operate in a tough space where upfront hardware costs and long payback periods curb fast valuation growth, yet they are crucial in a continent still wrestling with unreliable power. Investors are treating them like infrastructure plays with technology margins. Fintech still dominates, but the playbook is changing. Fintech retained the largest share of funding in 2025, and a new generation of payments and cross-border startups is stepping up. Honeycoin, for example, uses stablecoins to make cross-border payments simpler. Stablecoins are digital currencies pegged to traditional assets like the dollar so they avoid the wild price swings of many cryptocurrencies, making day-to-day business transfers more predictable. Honeycoin claims hundreds of thousands of users and substantial monthly flows, a sign that payments plumbing continues to attract both customers and investor interest. Beyond payments, startups such as Carschek in Nigeria are tackling long-standing market frictions, using artificial intelligence to bring trust and transparency to used-car markets through inspections and vehicle history verification. BAC Intelligence is applying data analytics to aviation, turning scattered datasets into decision tools for airlines and lessors. These are examples of companies targeting clear, monetizable problems rather than broad platform ambitions, a trend investors reward after the cautionary lessons of recent years. Agritech continued to show impact beyond headlines, helping cut post-harvest losses by 20 to 25 percent in some projects by using better market linkages and IoT tools. Startups in Nigeria and Kenya are connecting farmers directly to buyers, shortening supply chains and raising incomes. The wider tech ecosystem claims that the $4.1 billion in funding reported for 2025 translated into roughly 1.2 million jobs for people under 35, evidence that investment is producing tangible economic effect even as big exits slow. Deep tech and AI funding rose notably after showcases such as Morocco’s AFSIC and GITEX Africa spotlighted working products. Startups are training chip designers with university labs, building local language models for health chatbots, and using machine learning to optimize grids and agricultural yields. Corporate venture arms from large telcos like Safaricom and MTN have been active, buying equity where strategic data access matters. Deep tech is no longer just research, investors say; it is beginning to deliver contract revenues and piloted deployments. This digital transformation across sectors represents a fundamental shift in how technology is being deployed across the continent.

The Road Ahead for African Tech

The combined effect of faded froth and more sober funding is increased scrutiny. Investors now demand unit economics, repeatable sales channels, and early customer traction. Founders are scaling city by city, testing titles with small cohorts, and coming back to raise on the basis of clear metrics. Local venture funds have stepped up, filling about 40 percent of the capital gap left by global firms that pulled back. That alignment between domestic investors and founders helps startups survive longer and build models suited to local realities. But structural problems remain. Power reliability, measured in some indices as a score around 35 out of 100, constrains manufacturing and higher-value activities. Early-stage funding shortages persist in markets outside the main hubs, and geopolitical and regulatory uncertainty can stall cross-border expansion. IPO markets are also cautious after a year of stalled listings, so many exits are likely to be strategic sales or regional consolidations rather than immediate public offerings. The picture for 2026 is not a frothy sprint to new unicorn counts, but a steadier climb toward sustainable scale. The startups to watch are those that have demonstrated repeatable revenue models, aligned with evolving financing options, and plugged into regional hubs that can carry them across borders. Events and accelerator programmes are fast-tracking deep tech proofs, corporate VCs are providing both capital and distribution, and innovations that solve real economic pain points are returning investor attention. If these trends hold, 2026 could be the year African tech earns higher-quality exits and lays a foundation for a new generation of large, resilient companies. As detailed in BusinessDay’s analysis, the focus has shifted to sustainable growth rather than vanity metrics. Meanwhile, MohacAfrica’s comprehensive report highlights how these 18 contenders represent a more disciplined approach to scaling, and TechCrier’s watchlist shows similar patterns emerging across the ecosystem. This represents a significant evolution from the earlier boom periods we documented, suggesting Africa’s tech sector is entering a new phase of maturity and resilience.