African Startups Secure $174 Million in January 2026 as Fintech Leads and New Sectors Emerge

A Surprising Start to the Year

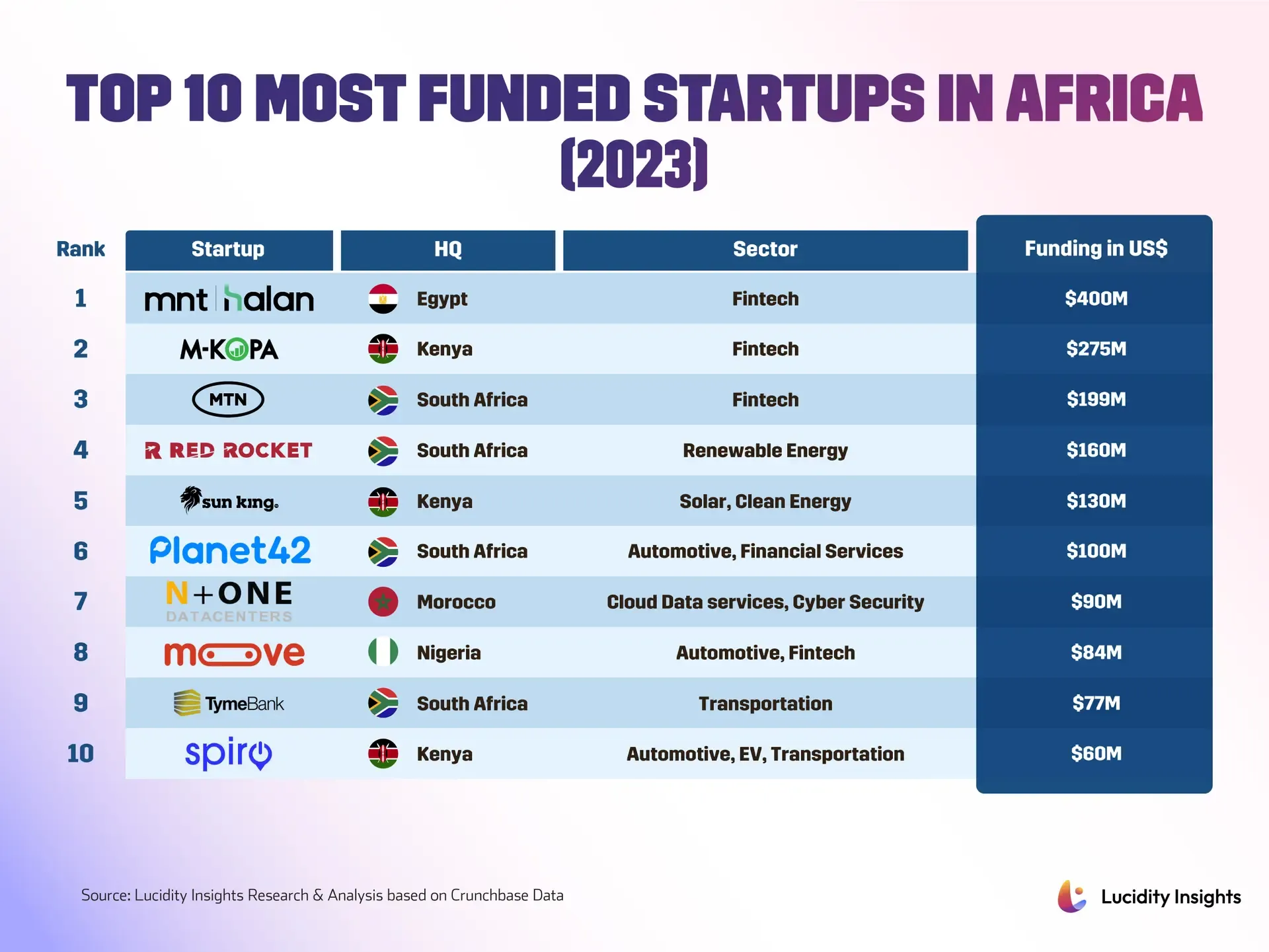

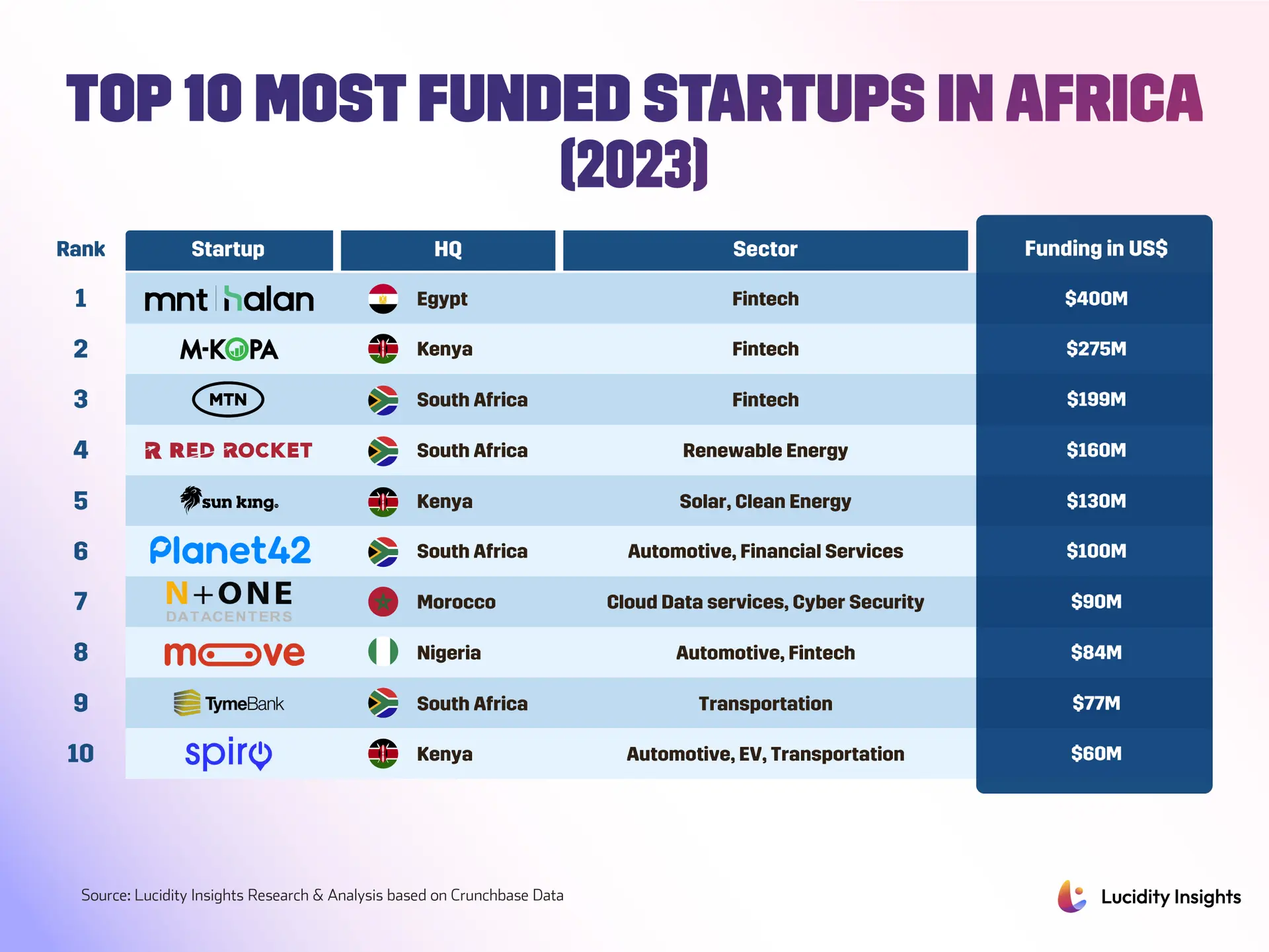

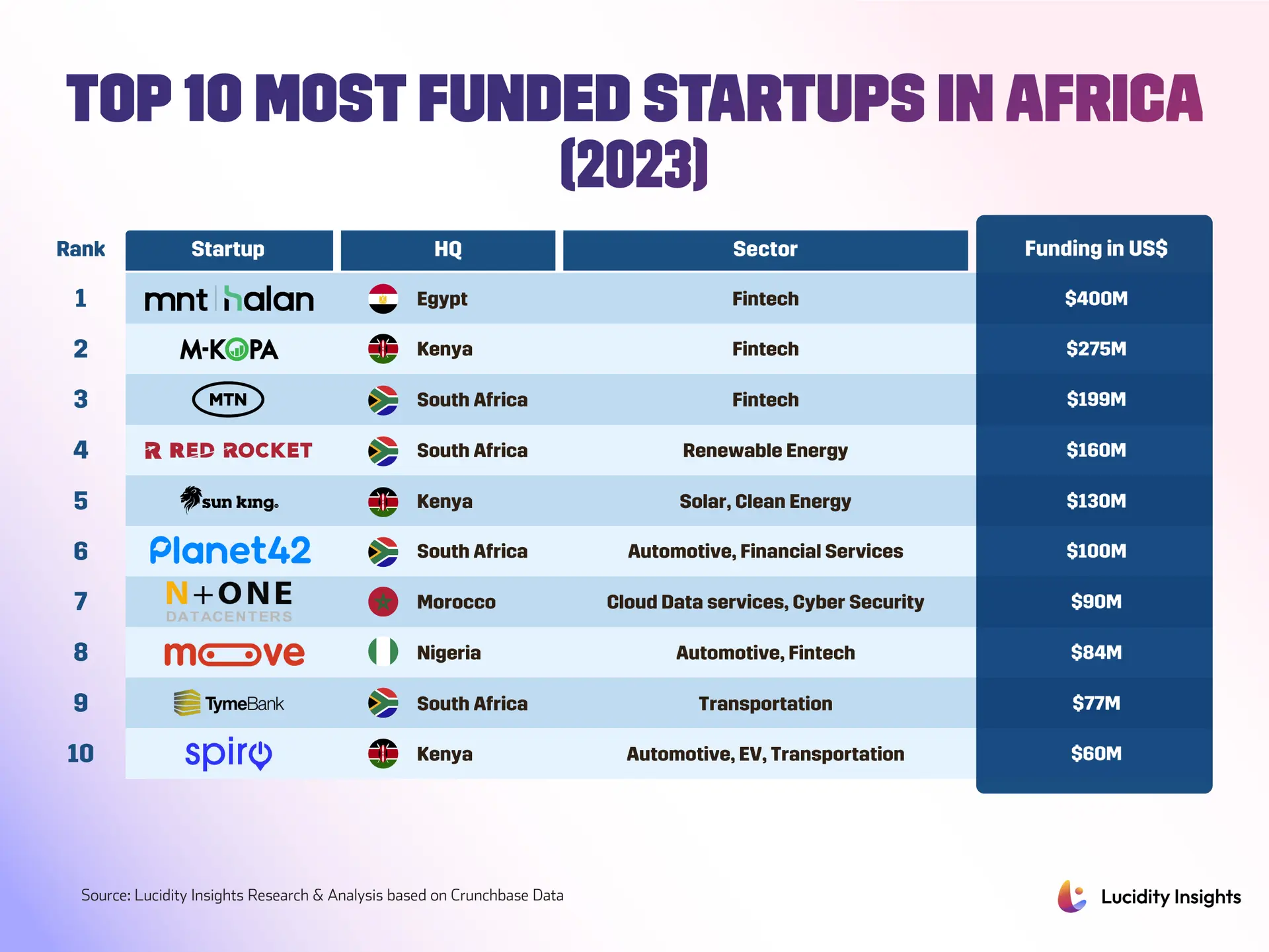

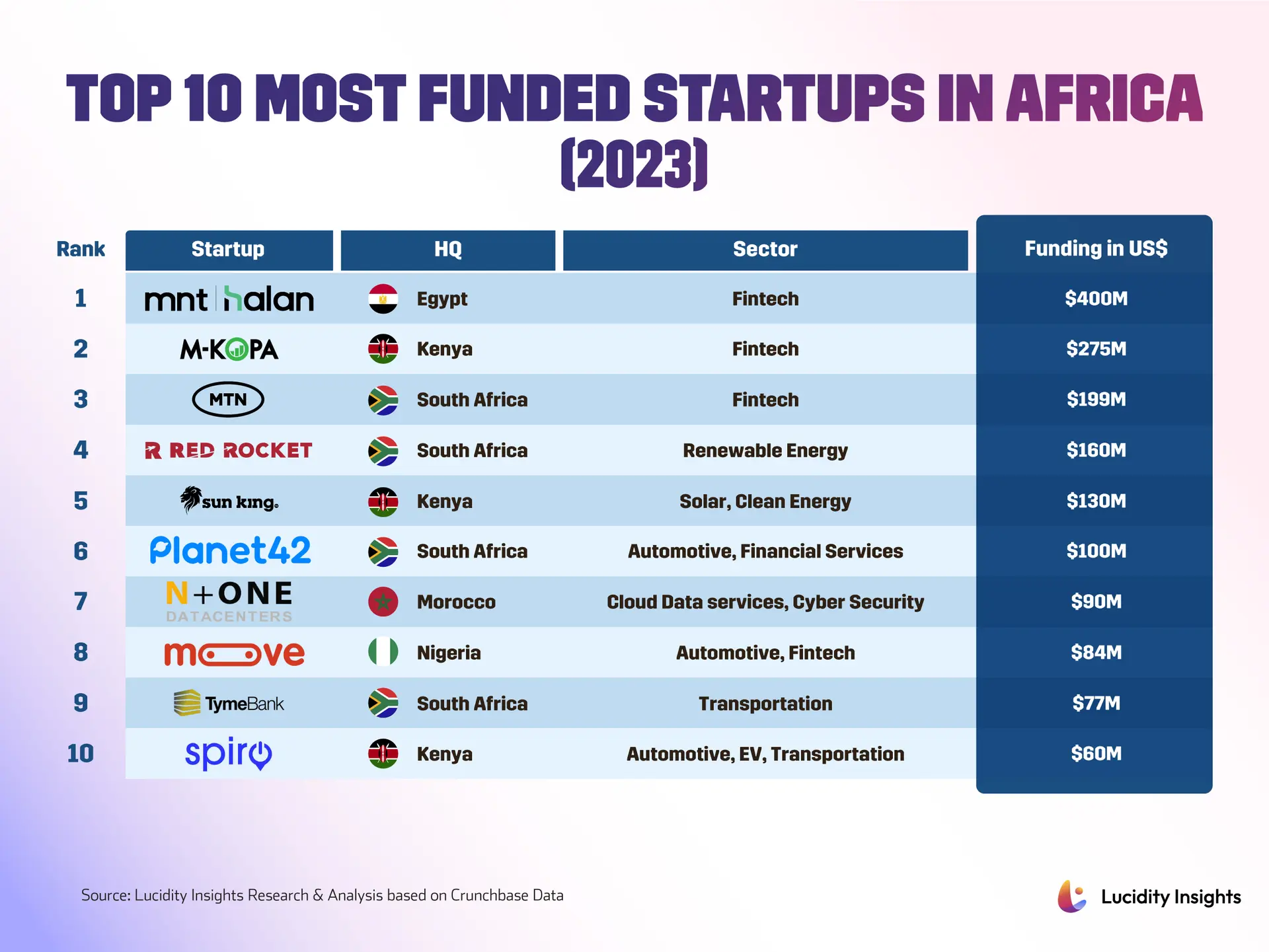

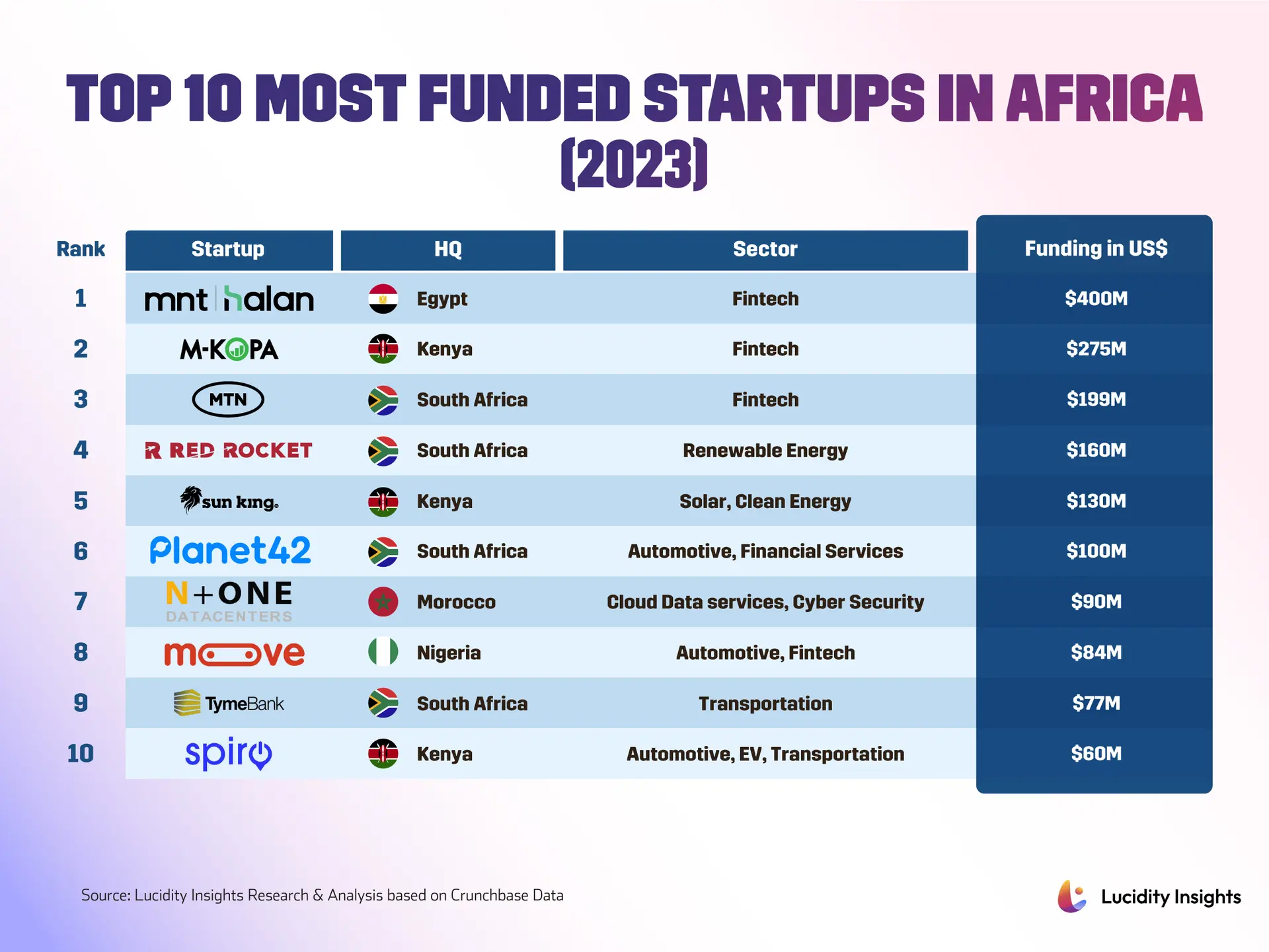

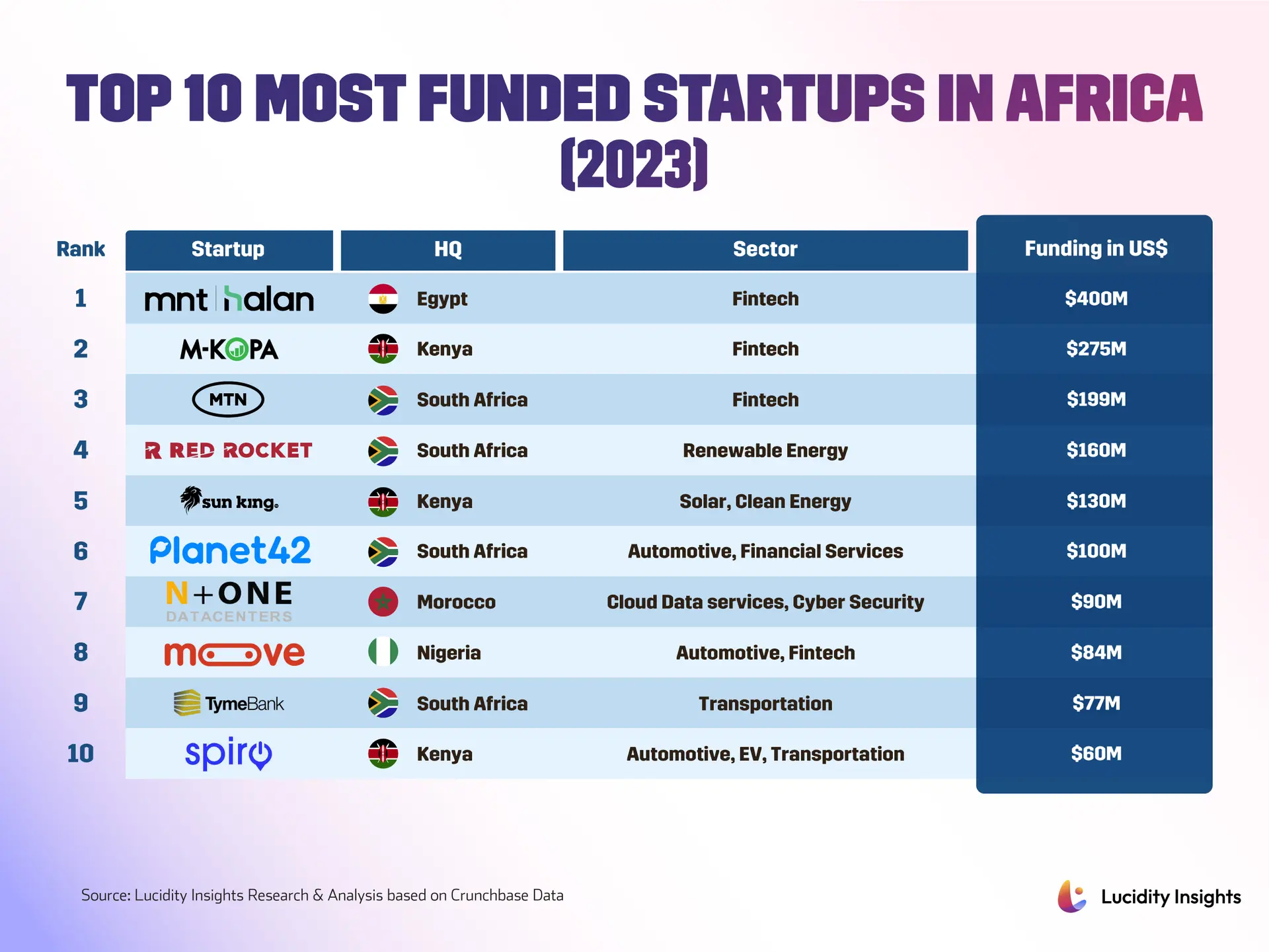

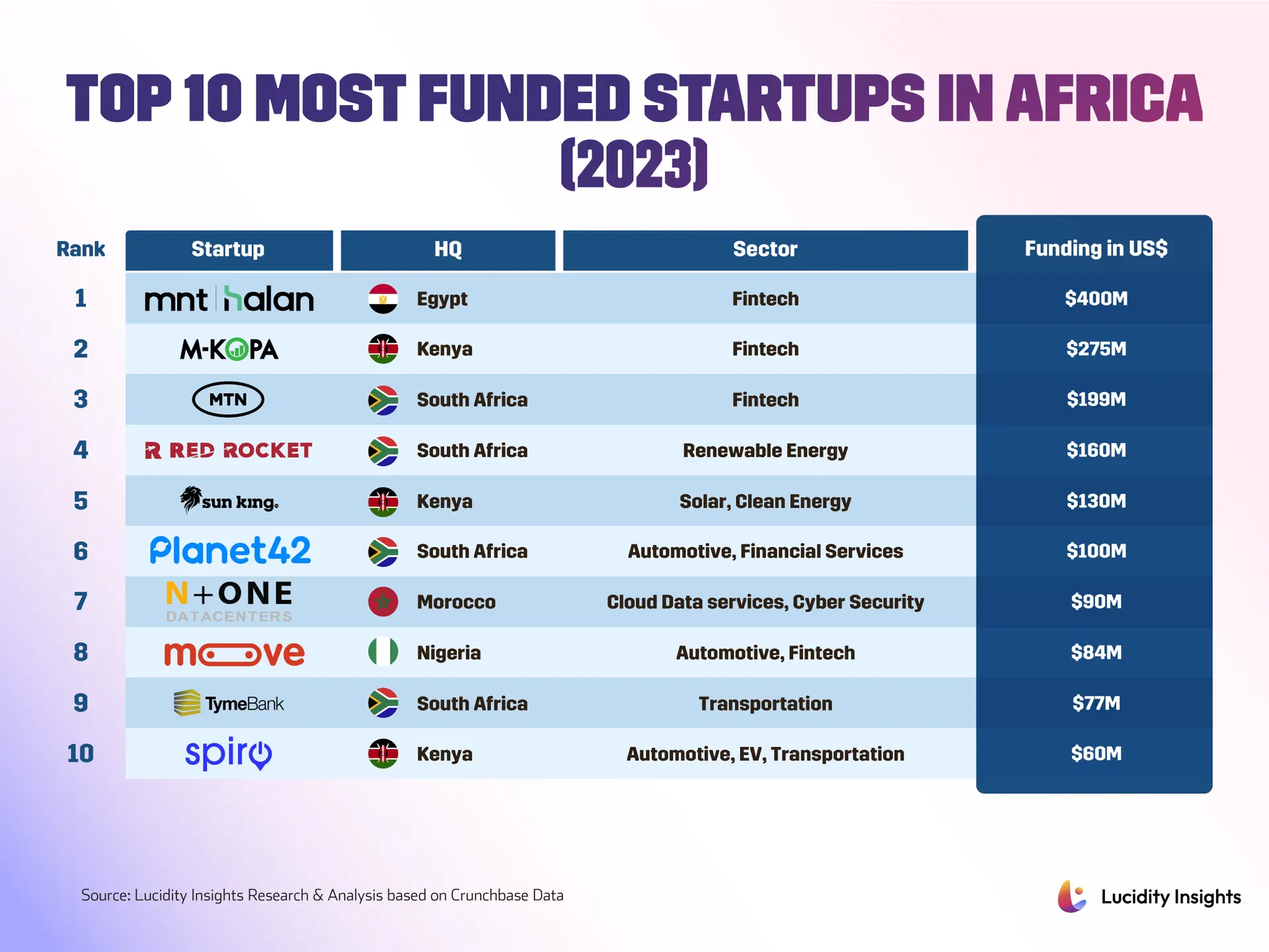

African startups kicked off 2026 by raising $174 million in disclosed funding during January, according to data from Africa: The Big Deal. At first glance, that figure might look like a step back from 2025’s monthly averages, but industry watchers caution against reading too much into a single month. Max Giacomelli, cofounder of the data platform, notes that slower January numbers aren’t unusual after December’s typical year end rush of large funding rounds. What’s really interesting isn’t the total amount but where the money’s flowing. Fintech remained the clear favorite, grabbing nearly 60 percent of January’s capital. That continued emphasis reflects investors’ longstanding belief that digital financial services and banking solutions for the underbanked still offer some of the fastest paths to scale across Africa’s diverse markets. The geography told a surprising story too. Egypt captured roughly half of the month’s funding, while traditional hubs like South Africa and Kenya stayed relatively quiet. Standout deals included Egypt’s The Value, which secured over $60 million, and Nigeria’s Max, which raised about $25 million. These transactions show how capital can cluster quickly around local champions that reach scale, and how national ecosystems can leapfrog each other as successful exits and large rounds emerge.

Beyond Fintech: New Frontiers and Local Capital

Investors aren’t just sticking to familiar territory. They’re showing renewed appetite for an expanding set of verticals beyond fintech. Sectors like proptech, which uses technology to reconfigure real estate markets, and defense tech, focused on territorial security and related technologies, are surfacing as emerging interests. This shift illustrates how Africa’s startup landscape is evolving from one defined by a handful of predictable categories to one that responds to real infrastructure needs, urbanization pressures, and national security priorities. A parallel and crucial development is the rise of local capital. A January report from Briter, highlighted in industry roundups, found that almost 40 percent of African startup funding now comes from local investors, up from roughly 25 percent just two years ago. Local investors bring more than money. They offer market knowledge, regulatory familiarity, and operational networks that foreign backers sometimes lack, and their increasing share can help de risk expansion across difficult regional borders. That regional integration is becoming a policy priority too. Afreximbank launched an accelerator targeting startups that enable intra African trade under the African Continental Free Trade Area, known as AfCFTA. The program selected eight tech startups for mentorship and potential equity support of up to about $250,000, aiming to fast track solutions that reduce friction in cross border commerce. Programs like this link capital to tangible trade objectives and can steer startup product roadmaps toward continental scale, much like the broader tech renaissance we’ve seen across the continent.

Maturing Markets and Future Trajectories

The broader funding environment shows clear signs of maturation. Tracxn’s mapping of the African startup landscape highlights a growing pipeline of exits and public listings, with companies like LeapFrog Investments and others moving to exchanges during late 2024 and 2025. Those exits help create recycling of capital through secondaries and new funds, a necessary ingredient for a deeper venture ecosystem. At the same time, investors are asking harder questions about unit economics and sustainable growth. African Business and other outlets have documented an intensifying scrutiny on returns, a natural consequence of the larger number of late stage rounds and public listings. This discipline, while uncomfortable for some founders, is a hallmark of a market moving from pure growth narratives to disciplined scaling. What does this mean for the rest of 2026? The first month’s numbers suggest a market that’s recalibrating. Fundraising seasonality, greater local investor participation, more measured investor due diligence, and the rise of new verticals are all reshaping how deals form. For founders, the message is clear. Product market fit and unit economics matter more than ever, and strategic partnerships with local capital can unlock growth across borders. For investors, the imperative is to balance conviction in high potential sectors like fintech with disciplined support for emergent areas. If January was a reset, the rest of 2026 will show whether this reset produces steadier growth, better matched capital, and more African champions listed or scaling across the continent. Watch for continued deal activity in Egypt and Nigeria, a steady stream of exits that recycle capital, and policy programs that aim to translate AfCFTA ambitions into real startup growth. The long view still favors a dynamic and diversifying African startup ecosystem, even as the market matures, building on the record growth we witnessed in previous years and continuing the momentum from when African startups soared with $1.4 billion in investment.