Africa’s Startup Rebound: A Reset, Not a Restart, as Companies Build for Profit and Scale

Across Africa, 2025 hasn’t felt like a fresh beginning so much as a careful reset. After two tough years of tightened capital and painful reckonings, deal activity and investment are climbing again, but the mood has shifted dramatically. Gone are the days of exuberant growth at any cost. Today’s ecosystem prizes disciplined scaling, solid unit economics, and clear paths to profitability. The result? A leaner, more selective landscape increasingly focused on building the physical and digital rails that other businesses will run on. Capital is returning, but on new terms. Data tracking the year shows deal activity up roughly a third compared with 2024, and total capital on pace to top $3 billion. Investors are back in the market, but they’re choosier than ever. The new wave of funding favors companies with recurring revenue, demonstrable unit economics (that’s the basic profitability of each customer or transaction after accounting for costs), and credible plans to reach break even. Backers want founders to show that the math works without perpetual fundraising. This shift has two immediate effects. It’s pushing startups to tighten spending and re-evaluate growth plans. And it’s elevating businesses that solve underlying infrastructure gaps, because these companies tend to generate more predictable revenue streams and can scale by selling platforms rather than one-off services. The continent’s startup ecosystem is clearly maturing.

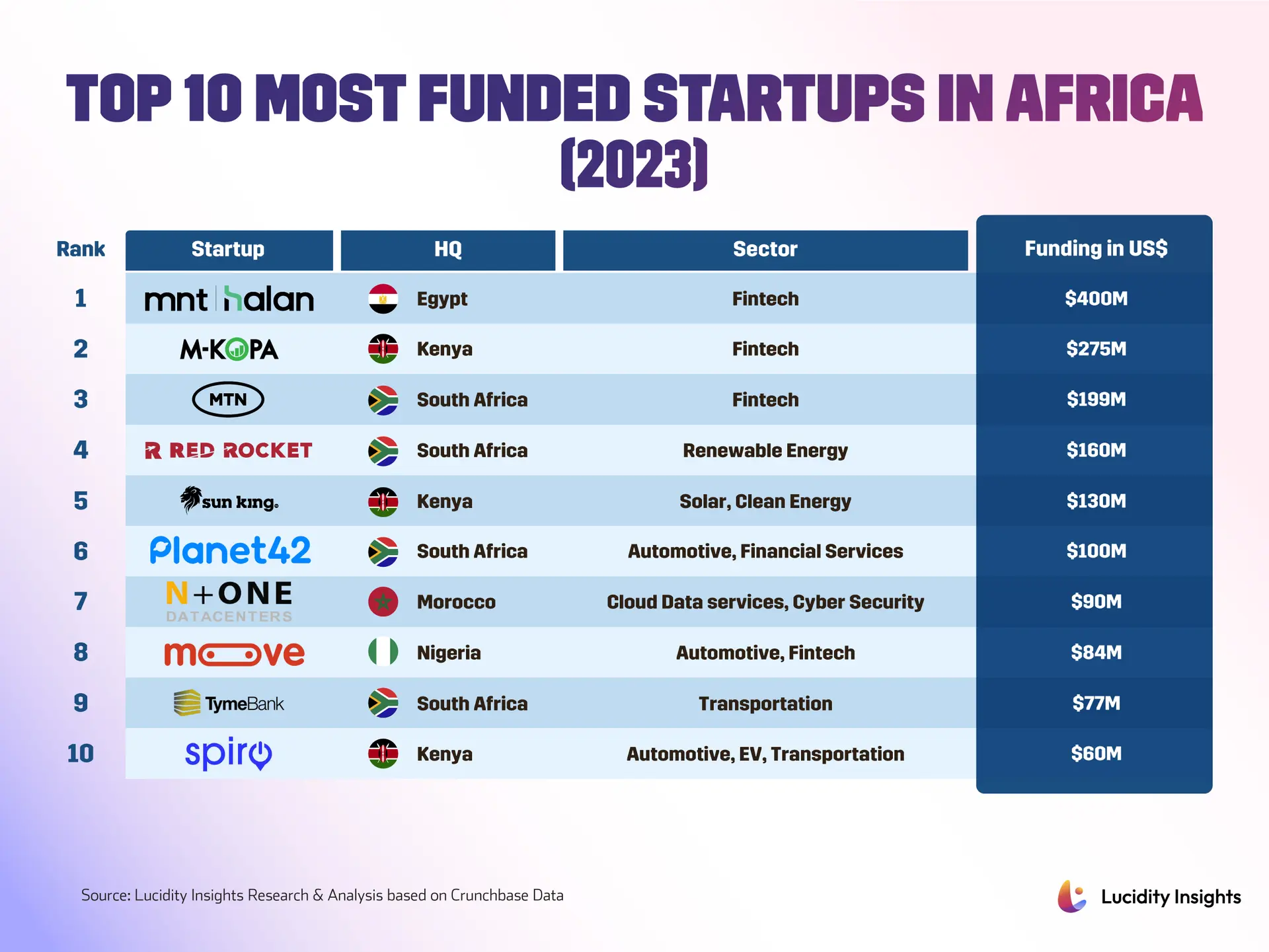

The startups drawing the most attention in 2025 are those laying Africa’s essential rails in finance, logistics, healthcare, energy and climate technology. These aren’t just another app or marketplace, they’re the plumbing that makes other services possible. Founders who can build payment systems, clinical data networks, reliable local logistics or distributed energy grids now command investor interest because their products create entire ecosystems. Industry lists compiled this year, like the one from African Business highlighting 20 such companies, reveal how African innovation is maturing. Rather than chasing rapid user numbers alone, these firms combine software, hardware and finance to solve long-standing operational problems, creating recurring revenue opportunities that appeal to risk-conscious investors. The period of correction that began in 2023 forced many founders to make hard choices. Layoffs were widespread, and while 2025 still saw workforce reductions, the pace has eased. Many cuts weren’t just about saving money, they were strategic reallocations, with teams trimmed to match healthier unit economics and new product priorities. Some prominent startups pivoted or narrowed focus, moving away from margin-thin consumer propositions toward business-to-business services, commodity traceability, and specialized logistics. These moves don’t necessarily signal failure. They reflect a learning curve: teams built for boom years were often overstaffed for a more disciplined market. Not every company survived the transition. A string of high-profile shutdowns this year reminded investors and founders that strong user metrics alone don’t guarantee sustainability. Some platforms with impressive engagement and mission-aligned goals closed because their revenue models couldn’t support operating costs, or because market timing didn’t match investor appetite for long-term paybacks. Those closures have sharpened conversations around sustainable business models and the need to align product ambition with clear monetization paths. One of the quieter revolutions unfolded in financial services, where stablecoins and blockchain-based solutions attracted both regulatory scrutiny and interest from commerce platforms. For African markets with high remittance volumes and fragmented payment systems, these tools hold promise, but regulators are increasingly involved, seeking to manage financial stability and consumer protection. This tech renaissance is reshaping the continent’s economic landscape.

Investors are doing more due diligence than ever, and that audit extends beyond unit economics to governance, compliance and regulatory risk. Publications tracking the ecosystem note a clear tightening of scrutiny from backers who now demand accountability and measurable performance. At the same time, policy developments, from cross-border trade considerations to carbon border taxes in global markets, are starting to factor into investment decisions for companies aiming at export-oriented growth, particularly in commodities and energy. Taken together, these dynamics paint a picture of an ecosystem transitioning from feverish expansion to structural maturation. The companies most likely to thrive are those that build essential infrastructure, prove unit economics early, and navigate regulatory headwinds with credible governance. That mix attracts patient capital, and it seeds platforms on which dozens of profitable, smaller businesses can be built. Looking ahead, the balance between capital availability and investor discipline will determine whether 2026 feels like a steady climb or another corrective year. Founders who use this moment to tighten unit economics, focus on recurring revenues, and invest in core operations rather than vanity metrics will be best placed to scale. For investors, the imperative is to back durable value creation that benefits customers and economies across the continent. As Forbes Africa reports, funding has rebounded significantly, while analyses like those from Weetracker provide sobering reminders about the challenges that remain. The continent’s startup funding surge signals renewed confidence, but it’s a confidence tempered by hard-won lessons from the recent past.