Africa’s Startup Boom Hits $1 Billion, But Growth Isn’t Equal

African startups just crossed a major threshold, pulling in more than one billion dollars from investors between January and May of 2025. That’s a roughly 40 percent jump from the same period last year, signaling that venture capital on the continent is moving beyond experimental bets toward more sustained investment. But that headline number tells only part of the story. Most of the new money still flows to the familiar quartet of Nigeria, Kenya, South Africa, and Egypt, where investors chase dense talent pools, large markets, and relatively clear regulations. A handful of second-tier capitals like Ghana, Tanzania, and Senegal are starting to attract regional attention, but the concentration of capital highlights both progress and a persistent imbalance.

Egypt’s Surge and the Fintech Engine

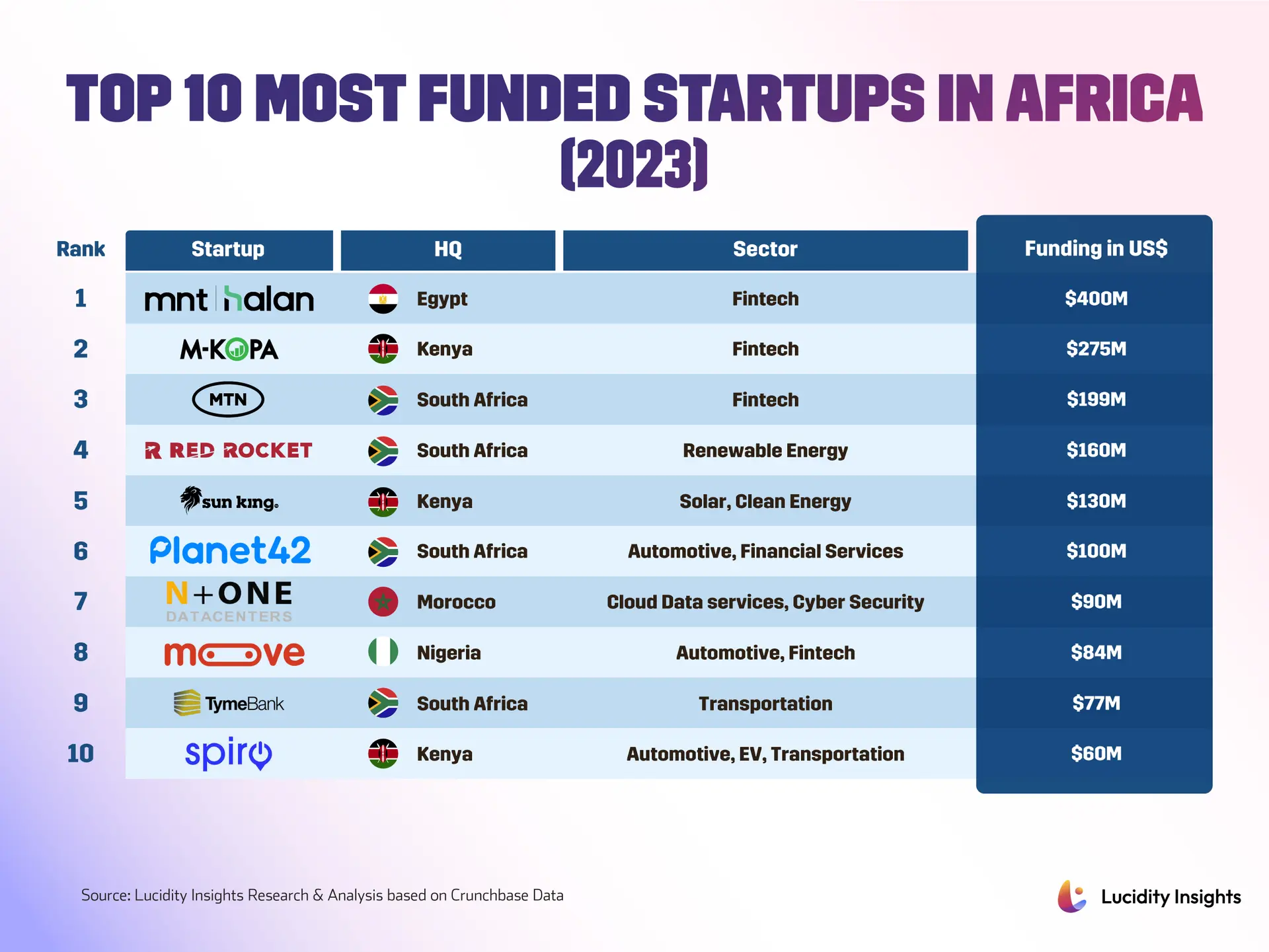

Egypt stands out as the breakout story of the moment. Funding activity there more than doubled in early 2025, driven by large rounds in property technology and financial technology. One Egyptian proptech company was among the continent’s biggest funding recipients in May, a clear sign that local startups are maturing and looking beyond their borders. Across Africa, fintech remains the dominant force, with companies reimagining payments, savings, and lending for informal economies drawing the most investor attention. They’re followed by startups in health, agriculture, and renewable energy. Investors are also placing fresh bets on electric vehicles and logistics, suggesting climate and transport tech can scale in African cities. But it’s not just about the quantity of money anymore. After years of enthusiastic early-stage investing, backers are now demanding clearer paths to profitability and stronger governance, pushing startups to sharpen their unit economics and prepare for tougher scrutiny.

Navigating Challenges and Building for the Future

The pressure for accountability comes alongside persistent structural hurdles. Many startups still face gaps in reliable power and affordable broadband, while uneven policy environments complicate cross-border expansion. Exit pathways remain limited in several markets, forcing investors and founders to build patient strategies. Yet the system is adapting. New funds focused on early-stage companies and specific sectors are emerging, offering local market knowledge alongside global networks. Corporate and development bank transactions are injecting liquidity into the broader economy, which indirectly benefits startups. Meanwhile, pockets of innovation outside traditional hubs are proving resilient, as founders in francophone West Africa and parts of East Africa build companies tailored to local needs. The tension between capital concentration and wider diffusion will shape what comes next. If money continues to cluster in a few markets, the most promising startups will accelerate, but many regions risk being left behind. A more balanced approach that combines marquee rounds with targeted investments in nascent ecosystems could create a wider base of high-potential companies. For founders, the path ahead means preparing for rigorous investor scrutiny and leveraging partnerships to scale across borders. For investors, it’s about blending return expectations with patient, hands-on support that acknowledges local realities. The one billion dollar milestone is cause for celebration, but it’s also a reminder that size alone doesn’t guarantee sustainability. Much depends on whether the ecosystem can translate this capital into repeatable success stories and resilient businesses that serve African customers at scale. If the current momentum holds and spreads, 2025 could be remembered as the year Africa moved decisively from promising experiments to a credible home for technology entrepreneurship and venture finance, as detailed in comprehensive startup listings and ongoing tech coverage.